SINGAPORE – More Singapore residents are hitting their Central Provident Fund (CPF) savings targets at age 55, according to the CPF Board’s 2025 annual report.

Such CPF members become eligible to withdraw excess savings if they wish. A record amount of withdrawable funds was taken out in 2025 by those aged 55 and above.

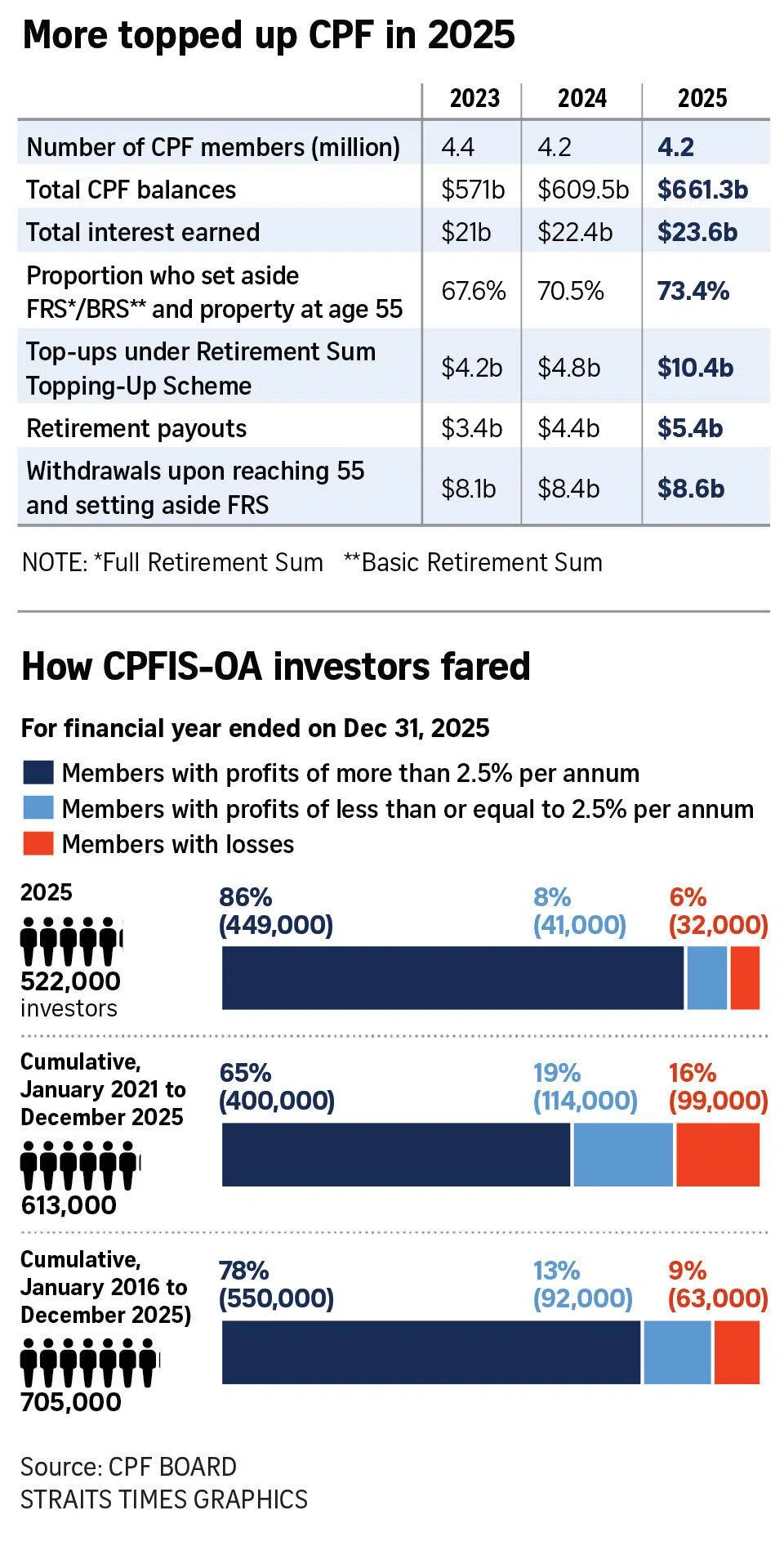

Of the 41,000 active CPF members who turned 55 in 2025, 73.4 per cent had set aside the Required Retirement Sum, up from 70.5 per cent in 2024.

This works out to 30,094 individuals whose Special Account savings had either hit the Full Retirement Sum (FRS) of $213,000 for their cohort, or had at least the Basic Retirement Sum (BRS) of $106,500 and owned a property.

An active CPF member refers to an individual who has at least one CPF contribution made for them for the current month or any of the preceding three months.

Self-employed individuals – such as hawkers, taxi drivers, freelancers, sole proprietors and partners in a partnership – are not considered active members unless they are also employees of a company.

Under key policy changes that took effect in January 2025, the CPF Board closed the Special Accounts (SA) for members aged 55 and above, to better align interest rates with the nature of savings in each CPF account.

SA savings were transferred to their Retirement Accounts (RA) up to each cohort’s FRS, to earn the long-term interest rate of at least 4 per cent a year.

Any remaining SA savings were transferred to their Ordinary Accounts (OA), which gives 2.5 per cent interest per annum. These savings can be withdrawn as needed or invested.

In 2025, such withdrawals reached a high of $8.6 billion.

Those who turn 55 and own a property with a remaining lease lasting until at least age 95 can choose to withdraw part of their Retirement Account savings down to the BRS.

They can withdraw up to $5,000 from their CPF savings, even if they are unable to set aside the FRS or the BRS using a property.

Boosting the RA balance gives members higher monthly payouts for life when they start their CPF LIFE payouts any time between the ages of 65 and 70.

So, instead of withdrawing their excess OA funds, some chose to transfer them to their RA to the Enhanced Retirement Sum (ERS) – a voluntary savings option that only becomes available when CPF members turn 55.

Top-ups can also be done in cash or CPF transfers by loved ones.

The ERS was increased in January 2025 to four times the BRS instead of three, or $426,000.

The raising of the ERS “spurred a significant increase in voluntary top-ups over $10.4 billion from 499,000 members, up from $4.8 billion the previous year”, CPF Board chairman Yong Ying-I noted in the annual report.

The report did not break down RA and SA top-ups, or cash top-ups and CPF transfers. Top-ups by members below the age of 55 go into their SA under the Retirement Sum Topping-Up Scheme.

The ERS increases every January, creating fresh headroom for members who had already reached the previous ceiling to make additional top-ups. The ERS became $440,800 in 2026, and will climb to $456,400 in 2027.

CPF said $5.4 billion was disbursed to 696,000 CPF members as retirement payouts in 2025, up 22.7 per cent from $4.4 billion in 2024.

This worked out to a simple average of about $647 per member a month, up from about $624 in 2024 and $552 in 2023.

Yong said retirement adequacy and financial security begin with informed choices made early.

She noted that more than 400,000 CPF members had accessed at least one of the financial planning features on the “PLAN (Plan Life Ahead, Now!) with CPF” platform launched in 2025.

Before they turn 55, members can invest their OA or SA savings into approved investments under the CPF Investment Scheme (CPFIS), as long as they keep $20,000 in their OA and $40,000 in their SA.

This could potentially allow them to earn more than the risk-free rate, which is 2.5 per cent for the OA and 4 per cent for the SA.

CPF members can continue to invest their OA under CPFIS after turning 55.

Existing SA investments can still be held after the SA is closed, but all their proceeds – including when these assets mature or are sold – will be paid to the RA up to the FRS.

Any remaining balance flows into the OA, giving members the flexibility to withdraw the cash, keep it in the OA, or reinvest it via CPFIS-OA.

For the year ended Dec 31 2025, 522,000 CPFIS-OA investors had investments, down from 544,000 in 2024, according to the CPF Board’s latest annual profit/loss report for CPFIS-OA investments.

About 86 per cent saw their investments outperform CPF’s OA interest rate of 2.5 per cent.

However, 8 per cent saw yields below or equal to the OA rate, and 6 per cent of the investors suffered total losses.

These figures were based on realised profits or losses of investments that were sold, as well as unrealised profits or losses of investments that members held during the reporting period.

Sixty-five per cent of the investors saw their cumulative profits over the five years from January 2021 to December 2025 beat the 2.5 per cent rate.

But 19 per cent had cumulative profits less than or equal to the OA interest rate, and 16 per cent made cumulative losses.

CPF Board chief executive Melissa Khoo said a new investment scheme will be launched in 2028 to give CPF members more options to grow their savings.

She said the scheme will cater to longer-term investors willing to bear some risk for potentially higher returns, but do not want to actively manage their investments.

{kind=link}