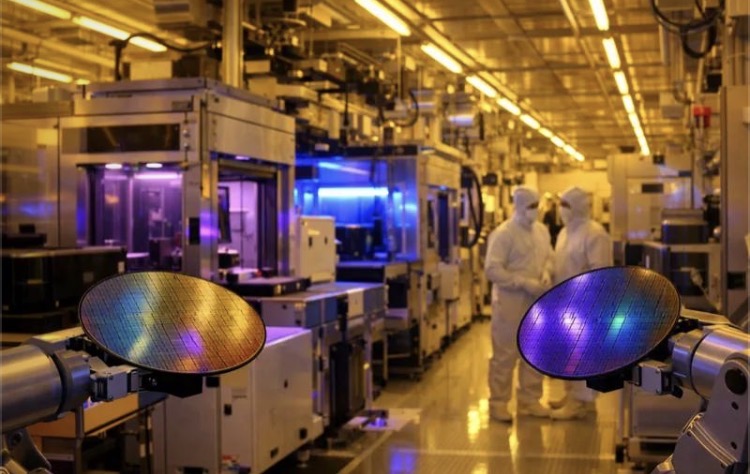

Investment in semiconductor manufacturing equipment is continuing to expand across Asia as chipmakers prepare for the next stage of advanced production, reinforcing the region’s role as the center of the global semiconductor supply chain.

Rather than focusing solely on increasing chip output, manufacturers are directing greater resources toward production efficiency, precision engineering and next-generation fabrication technologies. Industry analysts say the current investment cycle reflects a broader shift toward long-term manufacturing capability rather than short-term capacity expansion.

South Korea, Japan and Taiwan remain at the forefront of this transformation, supported by established semiconductor ecosystems and highly specialized engineering expertise. Equipment suppliers are strengthening partnerships with chip producers to improve manufacturing yields, reduce production costs and accelerate the commercialization of more advanced semiconductor processes.

International equipment manufacturers have also increased their presence across Asia by expanding technical support networks, research cooperation and customer service operations. As fabrication technologies become more complex, demand for localized engineering services and equipment maintenance has become increasingly important alongside hardware sales.

Governments throughout the region continue to view semiconductor manufacturing as a strategic industry. Public investment programs, workforce development initiatives and incentives for advanced manufacturing have encouraged both domestic and international companies to strengthen their regional operations. Policymakers increasingly regard semiconductor production not only as an economic asset but also as a key component of long-term industrial competitiveness.

The industry’s investment priorities are evolving alongside demand for artificial intelligence, high-performance computing and advanced automotive electronics. Modern chip production requires increasingly sophisticated manufacturing equipment capable of supporting smaller process technologies while maintaining high production reliability and quality standards.

At the same time, manufacturers continue to navigate challenges including rising development costs, supply-chain complexity and the need to secure highly skilled technical talent. Industry executives say maintaining technological leadership will depend as much on engineering capability and research collaboration as on capital investment alone.

Market observers believe Asia will remain the primary destination for semiconductor equipment investment over the coming years as governments and private companies continue strengthening regional manufacturing capacity. While the pace of expansion may vary with global economic conditions, demand for advanced production technologies is expected to remain a defining feature of the semiconductor industry.

For investors, the sector increasingly represents more than cyclical demand for electronics. Continued spending on manufacturing technology reflects confidence that semiconductors will remain essential to artificial intelligence, cloud computing, telecommunications and next-generation industrial applications, supporting long-term growth across the global technology sector.

SOPHIA KIM

US ASIA JOURNAL

{kind=link}